A.U.S.G. ’s New Report on Fossil Fuel Divestment, Summarized

On February 3, A.U. provost Daniel Meyers announced to several faculty members that A.U. had sold off a bundle of several funds managed by State Street Global Advisors (S.S.G.A.), which contained Carbon Underground 200 companies, and had re-invested in a suite of new funds which did not contain fossil fuels. Totalled $175 million and approved at the Board’s November 2019 meeting, the reinvestment involved in this exchange included the shedding of $6.9 million worth of carbon assets by means of a mechanism for divestment the Board had, five years ago, very publicly said was financially reckless.

As it currently stands, just 0.6 percent of the university’s endowment, or around $4.5 million, is invested in fossil fuels. In 2018, that figure was 2.7 percent, or some 18.8 million—a figure popularized by the #divest19million Fossil Free AU social media campaign two semesters ago. In 2014, when the Board of Trustees last considered divestment, it was 4.1 percent. That makes A.U. more divested than several major universities that have committed to divestment. One of these is Syracuse University, which screened out direct investments in fossil fuels in 2015 but still remains embedded in the industry via its commingled portfolio.

In both dollar value and percentage of the endowment, A.U. 's carbon ownership has fallen. The mechanism of selling and buying new stocks is nothing new, but in the context of fossil fuel divestment on college campuses across the U.S. and Europe, it is perhaps the cheapest one that works.

A Brief Flashback

It's good to know what happened the last time the Board considered divestment before reading about the push for the enactment of the policy this year. Here’s my extremely expedited timeline on what happened in 2014, derived from my last article on the subject, in which I unearthed a report whose story I now summarize so we can get to the cool stuff.

The campaign leading up to the vote in the Spring of 2014 began in the Fall of 2012 when leading members of Fossil Free A.U. first engaged in a series of meetings with President Neil Kerwin and Vice President for Campus Life Gale Hanson, as well as a number of trustees, including Jeff Sine. In mid-November of 2013, the Board chartered the Advisory Committee on Socially Responsible Investing to research the prospects of divesting from polluters for the Finance and Investment Committee, which advises the Board itself.

Members of the A.C.S.R.I. included a number of Fossil Free A.U. activists, many of whom were academically focused in environmental politics, as well as three faculty members: Prof. Paul Wapner, a professor of Global Environmental Politics in the School of International Service; Prof. Jeff Harris, a professor of Finance in the Kogod Business School; and Laura McAndrew, who served an advisory position as a key person in the administration’s Office of Finance.

Over six months, the A.C.S.R.I. report that served my starting spot in this research was produced around meetings with the Budget Office, personal research by the members of the committee, and presentations to Cambridge Associates, the university’s financial advisor at the time. According to committee members I interviewed, it became clear that Fossil Free A.U. 's priority was not necessarily to push this report as a core piece of the divestment campaign, but rather to build a strong coalition of student support on campus, which included the student body president, student trustee, and treasurer.

In January of 2013, 11 months before the A.C.S.R.I. was commissioned, Fossil Free A.U. circulated a petition to evaluate on-campus support of the divestment effort, as well as to bring the divestment issue to student government. The Undergraduate Senate passed the motion on a “Referendum on a Fossil Free American University” in March, and a campus-wide referendum was scheduled on April 2nd and 3rd. It passed with 79 percent of students in support. About a year later, on April 24, 2014, the A.C.S.R.I. report recommending divestment was formally submitted to the Finance and Investment Committee of the Board of Trustees, just in time for the Board’s meeting in May, which took place in Kay Spiritual Center.

On the day of the meeting, Fossil Free A.U. activists staged a sit-in outside the building. However, the Board did not vote on the divestment measure at that meeting. It was, instead, scheduled for the second of two meetings in November of 2014, which took place in the same building. Another rally was put on by activists, amassing the greatest body of student protesters the campus had seen in 50 years, a rally that notched a considerable spurt to the divestment movement across U.S. university campuses. As trustees were leaving, students blockaded the doors to prevent them from leaving.

Stranded Oil

A public forum was held on the same day of the meeting , where Neil Kerwin and Jeff Sine announced the decision of the Board to not enact the divestment measure. This decision came two days after Cambridge Associates had made a public release expressing its ability to explore prudent fossil-free investment avenues, seemingly endorsing the financial and legal legitimacy and salience of socially responsible investing. However, Jeff Sine wrote in a memorandum to the student body that Cambridge “could not provide assurance that divestment was unlikely to have an adverse effect” on the endowment and future returns, given that a) the combination of management expenses and transaction fees would levy too high a cost on the execution of the action, and b) the political nature of the action was, by definition, imprudent and could turn away potential donors that saw the university’s endowment managers as too politically engaged.

Several months after I published this article, I was invited to A.U.S.G Comptroller Bobby Zitzmann’s cabinet as Assistant Comptroller for Research. Our biggest initiative during the academic year would be a series of research reports on various university-related financial issues, authored by Bobby and myself, one of which included fossil fuel divestment. A key component in our recommendation was to express that time has sided with the world of socially responsible investing—or S.R.I., as I’m going to refer to it throughout this article—and that the Board should reconsider its position given new circumstances that have arisen in both these arenas: concern over investment returns, and playing privy to legally enscripted principles of fiduciary responsibility.

A very brief summary of our two pillars addresses these concerns most directly: first, the university’s carbon exposure had decreased through routine changes in investment tactics to a point where the effects of divestment were now placable, and second, since 2014, the domestic and international investing landscape had further shifted in favor of sustainable forms of energy—as it had been for decades before the Board voted no four years ago—to the point where the idea of oil and gas becoming what is called a stranded asset has now become common tongue within the financial industry.

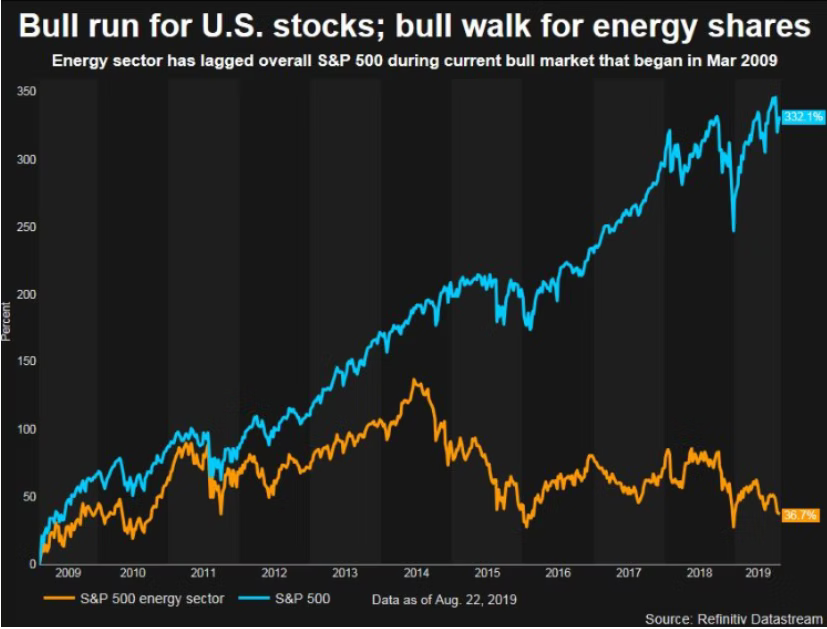

The energy industry experienced a dismal close at the end of fiscal year 2018 in August of last year. It clocked out as the worst-performing sector of the S&P 500 sectors since the start of the bull market that preceded the 2008 financial crisis and its brief aftershock two years after. Oil prices fluctuated with the market, but rallies were never the scale they were hoped to be. The energy sector as a whole performed even worse, according to Reuters columnist Lewis Krauskopf, “even [failing] to keep pace with oil prices, despite their traditional tendency to move in the same direction.” According to Greenwood Capital chief investment officer Walter Todd, “The view of the sector in general has gotten to a point where it’s a very difficult space for institutional investors to embrace because it’s been such a chronic underperformer.” Pearce Hammond, the Managing Director of Equity Research at Simmons Energy reportedly stated that “Investors have become wary of energy companies in the past out-spending their cash flows and of drilling wells without adequate returns.”

This negative trend isn't very old, but it isn't entirely new, either. Oil prices have been consistently disappointing for fossil fuel bulls. The S&P 500—along with the Dow Jones Industrial and N.A.S.D.A.Q.—is an index that most substantively represents the performance of the eleven sectors of the economy it tracks. The following graphic compares its energy company components to its overall performance.

The lagging of oil prices and the energy sector was a factor in the decision of the Norwegian government’s central bank to divest its $1.1 trillion sovereign wealth fund of oil explorers and producers, but keep refiners and other downstream firms on its portfolio. This is closely in line with the S&P 500 close just under a month earlier, which reported that the greatest stock winners of 2019 were Hess, Kinder Morgan, and Oneok, an oil refinery company, a pipeline and oil transportation company, and natural gas company, respectively. The greatest losers were all downstream firms. They included Cimarex, an oil production company based in Denver, as well as Halliburton and Concho Resources, both exploration companies.

The aptly named “carbon bubble” refers to the increasing volatility of carbon assets in a world that is increasingly hostile to its financial and political sustenance related issues. When the bubble “bursts,” so to speak, oil stocks will instantly turn toxic and oil prices worldwide will join in freefall. This is when oil becomes a “stranded asset,” a product that is unexpectedly devalued by exogenous forces.

Joel Makower—the chairman and executive director of GreenBiz Group, a firm committed to the intersection between business and sustainability—defines the term “stranded asset” as “a piece of equipment or a resource that once had value or produced income but no longer does, usually due to some kind of external change, including changes in technology, markets and societal habits.” Makower brings up the example of how whale oil became a stranded asset once electricity suddenly replaced oil lanterns as the popular option for lighting the home, and how the whaling industry “lost a key market for whale oil, leaving entire fleets idle.”

However, R. Andreas Kraemer, a senior fellow at the Institute for Advanced Sustainability Studies in Potsdam, argues a rather interesting point on this topic when it comes to fossil fuel companies and socially responsible investing. “Asset stranding results when assets have suffered from unanticipated or premature write-downs, devaluations or conversion to liabilities … nothing about climate change is unanticipated, and climate policy action is certainly not premature, but on the contrary fully predictable and overdue,” he writes. “Thus, there are no stranded assets in fossil energy companies caused by climate policy or the shift to green energy; any write-downs are the consequence of bad investment decisions and unjustified valuations, investments made in willful ignorance of the true costs and risks.”

Kraemer’s language here is important, and his case perhaps holds more merit than the common one. The idea that investing in fossil fuels has now become an incompetent position, instead of just a pessimistic one, gives the prospect of fossil fuel divestment more financial purpose—something it did not have that much of in 2014. Furthermore, today, we find the growth of the fossil-free investing sphere in the financial industry has increased exponentially over the last couple of years, with most substantive research literature on the topic reaching mainstream scholarship streams the same year the Board voted to reject divestment.

This growth, while only recently having seen its light in the mainstream, is not new. “The U.S. Forum for Sustainable and Responsible Investment estimates that assets managed according to S.R.I. discipline have grown from $600 billion in 1995 to $3.75 trillion in 2012,” writes Justin Marlowe in the Public Performance & Management Review, a prominent public administration journal. That figure has since increased to $6.5 trillion by 2018, according to Kate Stalter, who runs an asset management and financial planning firm.

Moreover, S.R.I. has been a growing sector of investment strategies that have blossomed in the last few ye